Paws and Paychecks: How I Tamed Pet Medical Bills with Smart Financial Tools

Ever had your heart drop when your dog needed emergency surgery? I did—and the vet bill hit like a truck. Suddenly, "pet parent" meant "unexpected financial planner." That’s when I discovered practical financial tools that don’t just save money, but peace of mind. No jargon, no get-rich-quick schemes—just real strategies that helped me handle pet medical costs without draining my savings. This is how I turned panic into preparation. What started as a crisis became a journey toward smarter money habits, one paw print at a time. And if you’ve ever stared at a veterinary invoice wondering how to pay it, you’re not alone.

The Moment It All Changed: When Fluffy Needed Surgery

It was a Tuesday evening when my golden retriever, Fluffy, collapsed in the backyard. One moment she was chasing a squirrel, full of energy; the next, she was whimpering, unable to stand. We rushed her to the emergency vet, where an ultrasound revealed a twisted stomach—a life-threatening condition requiring immediate surgery. The diagnosis came fast, but the cost estimate hit even faster: over $4,500. I stood in that fluorescent-lit exam room, clutching my wallet, realizing I didn’t have that kind of cash on hand. My emergency fund was meant for car repairs or job loss, not pet surgery. Yet there I was, facing a choice no pet owner wants to make—between my dog’s life and my financial stability.

This moment changed everything. Like many pet owners, I loved Fluffy like family. I bought her organic treats, took her to doggy daycare, and celebrated her birthday every year. But I never planned for the possibility of a major medical event. I assumed vet visits would be routine—annual checkups, vaccinations, maybe a bout of fleas. I didn’t anticipate advanced diagnostics, anesthesia, or overnight hospitalization. The reality is that modern veterinary medicine has evolved. Pets today receive treatments once reserved for humans: MRIs, chemotherapy, even orthopedic implants. These advances save lives, but they come with human-level price tags. A simple X-ray can cost $200; blood panels run $150 to $300; emergency surgeries often exceed $3,000. These aren’t outliers—they’re becoming standard.

What made the situation harder was the emotional weight. When your pet is in pain, logic takes a back seat. You’ll do almost anything to help them. That instinct is beautiful, but it can lead to financial strain when unprepared. I wasn’t reckless—I had a budget, savings, and decent credit. But I hadn’t included pets in my financial planning. Fluffy’s surgery wasn’t just a medical crisis; it was a financial wake-up call. It forced me to confront a truth many pet owners ignore: loving your pet means preparing for their health needs, not just their daily comforts. The love is free, but the care isn’t. And pretending otherwise risks both your pet’s well-being and your own financial security.

Why Pet Medical Expenses Are a Silent Budget Killer

Pet medical costs are one of the most underestimated expenses in household budgeting. Unlike car payments or mortgage bills, they’re irregular and unpredictable. You can’t set a fixed monthly amount because you never know when a pet might eat a sock, step on a nail, or develop a chronic illness. This uncertainty makes them easy to overlook—until the bill arrives. And when it does, it often feels like a punch out of nowhere. Yet these costs aren’t random. They’re the result of deeper trends in pet ownership and veterinary care. Understanding these forces is the first step toward managing them.

One major factor is inflation in veterinary services. Over the past decade, the cost of pet healthcare has risen steadily, mirroring trends in human medicine. Veterinary clinics invest in advanced equipment, specialized training, and facility upgrades—all of which increase operating costs. These expenses are passed on to pet owners. At the same time, treatment options have expanded. Where once a limping dog might have been sent home with rest and painkillers, today’s vets can offer diagnostics like MRIs, physical therapy, or even stem cell treatments. These options improve outcomes, but they also increase the financial stakes. A pet owner now faces not just medical decisions, but financial ones: Is surgery worth the cost? Can we afford long-term medication? Should we pursue every possible test?

Another reason these costs catch people off guard is psychological. We see our pets as family members, not financial liabilities. We don’t buy life insurance for our children or set up retirement accounts for our spouses—and so we don’t think to plan for their medical emergencies either. This emotional framing makes it hard to approach pet care with financial discipline. When a crisis hits, we react emotionally, not strategically. We say yes to treatments because we love our pets, not because we’ve budgeted for them. The result is often debt, drained savings, or difficult choices. The problem isn’t overspending—it’s the absence of planning. Pet medical expenses aren’t outliers; they’re foreseeable risks. And like any risk, they can be managed with the right tools and mindset.

Emergency Fund? Not Just for Humans Anymore

After Fluffy’s surgery, I made one simple but powerful change: I opened a dedicated pet emergency fund. This isn’t a complex investment strategy or a high-risk financial product. It’s a separate savings account, earmarked solely for unexpected pet expenses. The idea is straightforward—set aside small amounts regularly so that when a crisis occurs, you’re not scrambling for cash. This fund became my financial safety net, and it’s one of the most effective tools I’ve used to regain control. Unlike general savings, which can be tempted by vacations or home repairs, a pet-specific fund keeps the purpose clear and the money protected.

Starting this fund didn’t require a big upfront deposit. I began with $50, then set up an automatic transfer of $75 from my checking account every payday. That’s less than $20 a week—about the cost of a few takeout meals or a streaming subscription. Over time, those small contributions added up. Within a year, I had over $1,200 saved. When Fluffy needed a dental cleaning six months later—a $600 procedure—I paid it without touching my main savings or using credit. That sense of relief was priceless. The key is consistency, not size. Even $25 a month builds a $300 buffer in a year. For older pets or breeds prone to health issues, you might increase the amount, but the principle remains the same: small, regular savings prevent large, stressful payments.

Where you keep this fund matters too. I chose a high-yield savings account, which earns more interest than a traditional bank account. It’s still liquid, so I can access the money quickly if needed, but it grows slightly over time. Some people use separate physical envelopes or digital budgeting apps to track pet savings—what matters is that the money is set apart and not mixed with other expenses. The psychological benefit is just as important as the financial one. Knowing there’s a fund in place reduces anxiety. You’re no longer facing the unknown; you’re working from a position of preparedness. This shift—from fear to control—is where real financial peace begins. A pet emergency fund doesn’t guarantee you’ll never face a tough decision, but it ensures that money won’t be the only factor.

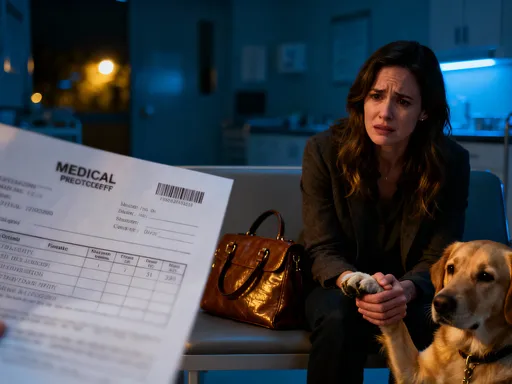

Pet Insurance: Worth It or Waste of Cash?

Pet insurance was a concept I dismissed at first. It sounded like another monthly bill with no immediate benefit. But after Fluffy’s surgery, I started researching. What I found was a nuanced picture. Pet insurance isn’t a magic fix, but for many owners, it can be a valuable part of a financial strategy. The basic model is similar to human health insurance: you pay a monthly premium, and in return, the insurer covers a portion of eligible veterinary costs. Policies vary, but most cover accidents, illnesses, surgeries, and sometimes hereditary conditions. Routine care—like vaccinations or teeth cleanings—usually requires an add-on plan.

My first attempt at getting coverage was a lesson in timing. I applied when Fluffy was seven years old, already past the ideal enrollment window. The insurer accepted her, but with exclusions for hip and joint issues—common in golden retrievers. When she later developed arthritis, those treatments weren’t covered. I had paid premiums for two years but received little benefit. That experience taught me a crucial rule: the earlier you enroll, the better. Most insurers offer lower rates for younger, healthier pets and cover a broader range of conditions. Waiting until a pet shows symptoms often means pre-existing conditions are excluded, reducing the policy’s value.

I didn’t give up. I compared plans, read customer reviews, and studied the fine print. Eventually, I found a provider with transparent terms, reasonable premiums, and a claims process that reimbursed within two weeks. I now have coverage for my new puppy, Luna, who’s covered for everything from ear infections to emergency surgery. I’ve filed three claims so far—for a swallowed toy, a skin allergy, and a minor injury—and been reimbursed for over 80% of the costs. The savings add up. Still, pet insurance isn’t for everyone. It requires discipline to pay premiums even when no claims are made. And it doesn’t cover everything—deductibles, co-pays, and coverage limits still apply. But for those willing to plan ahead, it can significantly reduce the financial shock of a medical crisis. The real value isn’t in getting rich—it’s in staying solvent while giving your pet the care they need.

Credit Options That Won’t Break You

Not every pet owner can save thousands in advance or afford monthly insurance premiums. That’s where responsible credit use comes in. When Fluffy needed surgery and my savings fell short, I turned to CareCredit, a medical credit card designed for health expenses, including veterinary care. It offered six months of no interest if paid in full. I qualified, charged the remaining $2,000, and set up a repayment plan that fit my budget. By paying it off within the promotional period, I avoided interest entirely. This tool gave me breathing room when I needed it most. But I know it could have gone differently. Had I missed the deadline, the interest rate would have retroactively applied, turning a manageable debt into a costly one.

CareCredit and similar programs can be lifelines, but they require caution. These are not everyday credit cards. They’re specialized financial products with strict terms. The no-interest period is only a benefit if you can repay the full balance on time. Otherwise, high interest rates—sometimes over 25%—kick in, making the debt hard to manage. I’ve seen pet owners get trapped in cycles of minimum payments, where they’re barely chipping away at the principal. That’s why I treat medical credit like a loan, not a convenience. I calculate the monthly payment I can afford, set reminders for due dates, and treat it as a fixed expense, just like a car payment.

Personal loans are another option. Some banks and credit unions offer unsecured loans for pet expenses, often at lower fixed rates than credit cards. These provide predictable payments over time and don’t carry the risk of retroactive interest. However, they require a credit check and approval process, which can take days—too slow for a true emergency. That’s why I recommend having a plan in place before disaster strikes. Know your credit score, pre-qualify for loan options, and understand the terms. Credit should never be the first line of defense, but it can be a reliable backup when combined with savings and insurance. The goal isn’t to avoid debt at all costs, but to use it wisely, intentionally, and temporarily.

Budgeting Hacks Every Pet Owner Should Know

Beyond emergency funds, insurance, and credit, there are everyday strategies that help manage pet costs without sacrificing care. These aren’t flashy or complex, but they add up over time. One of the most effective is bundling wellness services. Many vets offer annual packages that include exams, vaccines, flea prevention, and dental checks at a discounted rate. Paying upfront for a year’s worth of care can save 15% to 20% compared to paying per visit. I switched to a wellness plan for Luna, and it’s cut my out-of-pocket costs significantly. Even better, it encourages preventive care, which can catch problems early—before they become expensive emergencies.

Another simple hack is asking for cash discounts. Some clinics charge less if you pay with cash or debit, since it avoids credit card processing fees. I’ve saved $50 on a single visit just by switching payment methods. It’s not advertised, so you have to ask. Similarly, I always request generic medications when available. Just like in human medicine, generic versions of common drugs—like antibiotics or anti-inflammatories—work just as well but cost far less. My vet was happy to prescribe them once I asked. I’ve also learned to shop around for supplies. Buying heartworm prevention or flea collars online, in bulk, or during sales can save hundreds a year.

For low-income families, nonprofit assistance programs can be a game-changer. Organizations like the Humane Society, Red Rover, and local animal welfare groups sometimes offer grants or low-cost clinics for urgent care. These aren’t handouts—they’re resources designed to keep pets with their families. I’ve referred friends to these programs, and they’ve received help with surgeries, cancer treatments, and chronic disease management. The key is knowing they exist and applying early. These tools don’t replace financial planning, but they complement it. Together, they form a layered approach: prevention, savings, insurance, credit, and community support. No single strategy is perfect, but used together, they build resilience.

Building a Long-Term Plan: From Reactive to Proactive

The biggest shift in my financial life wasn’t a single tool—it was a mindset change. I moved from reacting to crises to preparing for possibilities. Today, my pet care strategy combines multiple layers: a growing emergency fund, active insurance for my younger dog, and a clear understanding of credit options if needed. I review this plan annually, adjusting for my pets’ ages, health, and my own financial situation. When Luna turned five, I increased her insurance coverage. When Fluffy entered her senior years, I boosted her emergency fund contribution. These aren’t one-time decisions—they’re ongoing practices.

Creating your own plan starts with honesty. Ask: What’s my risk tolerance? How much can I afford to save each month? What kind of care do I want to provide, regardless of cost? For some, that means full insurance and a $5,000 fund. For others, it might be a smaller cushion and reliance on preventive care. The right plan fits your life, not someone else’s. I encourage pet owners to assess their pet’s life stage—puppies and kittens benefit most from early insurance; seniors need stronger savings. Income stability matters too. If your job is unpredictable, a larger emergency fund may be wiser than a fixed premium.

The goal isn’t perfection. It’s progress. You don’t need to have everything figured out today. Start with one step: open a savings account, research one insurance quote, or set a monthly reminder to save $20. Small actions build momentum. Over time, they create a safety net that lets you make medical decisions based on love, not limits. That’s the real win. Financial tools don’t just protect your wallet—they protect your peace of mind. They ensure that when your pet needs you, you’re ready—not just with affection, but with resources.

Peace of Mind Is the Best Investment

Managing pet medical costs isn’t about getting rich. It’s about staying in control. It’s about looking into your dog’s eyes after a diagnosis and knowing you can do right by them without wrecking your finances. The strategies I’ve shared—emergency funds, insurance, smart credit, and budgeting hacks—aren’t secrets. They’re accessible, practical tools available to anyone who loves a pet. They don’t promise miracles, but they deliver something more valuable: stability. The real return on these investments isn’t measured in dollars saved, but in confidence gained. It’s the quiet assurance that you’re prepared, that you won’t have to choose between your pet’s health and your financial future. In the end, that peace of mind is the best reward of all. And it’s one worth every penny.